Smart money habits are essential for anyone looking to achieve financial stability and success. In today’s fast-paced world, understanding how to manage your finances effectively can make a significant difference in your overall well-being. From budgeting to investing, the habits you form can set you on a path to a secure financial future.

This comprehensive guide explores various aspects of personal finance, including effective budgeting techniques, the importance of financial planning, and smart investing strategies. By embracing these smart money habits, you can take control of your finances and work towards achieving your financial goals with confidence.

Smart Money Habits

Establishing smart money habits is essential for achieving financial security and independence. With a solid approach to managing finances, individuals can avoid unnecessary debt, build savings, and ultimately reach their financial goals. This guide will delve into the importance of budgeting, effective expense tracking, and tips for setting achievable financial goals.

Importance of Budgeting for Financial Stability

Budgeting serves as the foundation of financial stability. It involves creating a plan that Artikels income and expenses, allowing individuals to control their finances effectively. By consistently tracking where money goes, one can identify areas for savings and adjust spending habits accordingly. A well-structured budget can help in avoiding overspending and ensures that funds are allocated toward essential expenses and savings.

“A budget is telling your money where to go instead of wondering where it went.”

Creating a budget requires a comprehensive understanding of fixed costs (like rent and utilities), variable expenses (such as groceries and entertainment), and savings goals. By regularly reviewing and updating the budget, individuals can adapt to changes in their financial situations, ensuring ongoing stability.

Methods for Tracking Personal Expenses Effectively

Tracking personal expenses is crucial for maintaining a budget and understanding spending patterns. There are various methods to do so, each with its own advantages:

- Mobile Apps: Numerous apps are available that automate expense tracking, making it convenient to categorize and monitor spending in real-time. Examples include Mint, YNAB (You Need a Budget), and PocketGuard.

- Spreadsheets: For those who prefer a more hands-on approach, creating a customized spreadsheet in programs like Excel or Google Sheets allows for detailed tracking and easy analysis of financial data.

- Pencil and Paper: Some individuals find that simply writing down expenses in a notebook helps reinforce their spending habits, creating a more tangible connection to their finances.

Regardless of the method chosen, the key is consistency. Regularly updating expense records empowers individuals to make informed decisions about their financial habits and identify areas for improvement.

Tips for Setting and Achieving Financial Goals

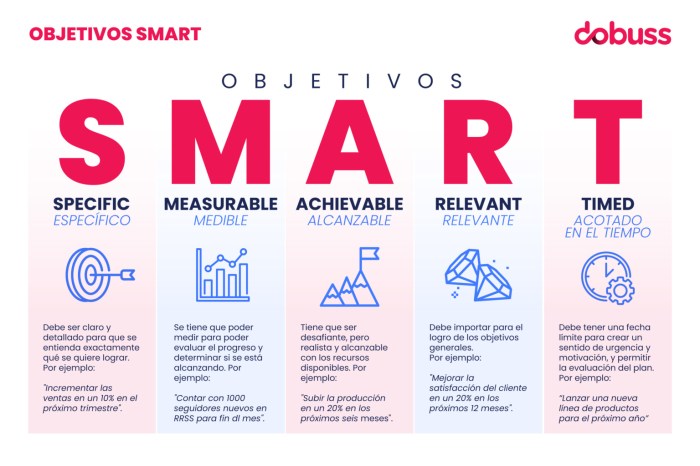

Establishing clear financial goals is vital for long-term success. Whether saving for a vacation, building an emergency fund, or planning for retirement, setting specific, measurable, attainable, relevant, and time-bound (SMART) goals can enhance focus and motivation.To effectively achieve these goals, consider the following strategies:

- Define Clear Objectives: Identify what you want to achieve and set a detailed plan with timelines. For instance, instead of stating a vague goal like “save money,” specify “save $5,000 for a down payment by December 2024.”

- Break Down Goals: Divide larger goals into smaller, manageable steps. This approach makes the process less daunting and allows for regular progress checks.

- Automate Savings: Set up automatic transfers to a savings account dedicated to your goals. This method ensures consistency and helps in building savings without the temptation to spend.

- Review Progress Regularly: Schedule periodic reviews of your financial goals to assess progress and make necessary adjustments based on changing circumstances or priorities.

Taking these steps can lead to increased financial discipline and a better chance of achieving long-term financial aspirations.

Financial Planning

Creating a comprehensive financial plan is vital for achieving long-term financial stability and meeting personal goals. A well-structured financial plan helps individuals understand their current financial situation, set realistic goals, and implement strategies to achieve those goals. This process involves a series of steps that ensure a holistic approach to managing finances effectively.The first step in financial planning is assessing your current financial situation.

This includes evaluating income, expenses, assets, and liabilities. Understanding where you stand financially allows you to identify areas for improvement and set realistic goals. Next, it’s essential to set clear, measurable, and achievable financial goals, whether they pertain to saving for retirement, buying a home, or paying off debt. After establishing goals, the next step is to create a budget that aligns with your financial objectives, making sure it reflects your income and necessary expenditures.

Steps to Create a Comprehensive Financial Plan

Developing a financial plan involves several key steps that guide individuals toward effective financial management.

- Assess Current Financial Situation: Review your income, expenses, assets, and liabilities to understand your financial health.

- Set Financial Goals: Define specific, measurable, and time-bound financial objectives that reflect your needs and aspirations.

- Create a Budget: Develop a detailed budget that allocates funds toward various expenses while allowing room for saving and investment.

- Identify Investment Opportunities: Evaluate different investment options based on your risk tolerance and financial goals.

- Monitor and Adjust Your Plan: Regularly review your financial plan to ensure it remains aligned with your goals and make adjustments as needed.

Utilizing tools and resources can significantly enhance the effectiveness of financial planning. Various budgeting apps, investment platforms, and online calculators are available to simplify the planning process.

Tools and Resources for Financial Planning

A variety of tools and resources can assist individuals in creating and managing their financial plans effectively.

- Budgeting Software: Applications like Mint or YNAB (You Need A Budget) help track expenses and manage budgets in real-time.

- Investment Platforms: Services such as Robinhood or E*TRADE provide easy access to stock and bond investing.

- Financial Calculators: Online calculators can assist with mortgage calculations, retirement savings, and budgeting.

- Books and Courses: Financial literacy improves with resources like “The Total Money Makeover” by Dave Ramsey or online courses offered through platforms like Coursera.

The role of an emergency fund in financial planning cannot be overstated. An emergency fund serves as a financial safety net, ensuring that unexpected expenses do not derail your financial goals.

Importance of Emergency Funds

Establishing an emergency fund is a critical aspect of financial planning, as it provides security and peace of mind during unforeseen circumstances.

An emergency fund should ideally cover three to six months’ worth of living expenses.

Having a dedicated fund for emergencies helps in several ways:

- Reduces Financial Stress: Knowing you have a cushion for unexpected bills can alleviate anxiety during tough times.

- Prevents Debt Accumulation: Access to an emergency fund can prevent reliance on credit cards or loans when unexpected expenses arise.

- Supports Long-Term Goals: A well-maintained emergency fund allows for focus on long-term savings and investment goals without interruptions.

Financial planning is an ongoing process that requires regular reflection and adjustment to stay on track toward your objectives. By following structured steps, utilizing helpful tools, and maintaining an emergency fund, individuals can build a robust financial future.

Investing Strategies

Investing is a crucial component of financial planning and can significantly shape your financial future. For beginners, navigating the investment landscape can be overwhelming, but understanding basic investment options and strategies can make the journey smoother. This section will Artikel various investment options suitable for newcomers, provide a comparison of key investment types, and guide on assessing one’s risk tolerance before diving into the market.

Investment Options for Beginners

New investors have a variety of options to consider when starting their investment journey. It’s essential to choose investments that align with your financial goals, risk tolerance, and time horizon. Here are some common investment types:

- Stocks: Buying shares of a company gives you ownership and the potential for capital appreciation and dividends.

- Bonds: These are loans made to corporations or governments, providing interest income and repayment of principal over time.

- Mutual Funds: Pooled funds managed by professionals that invest in a diversified portfolio of stocks and/or bonds, making them suitable for those wanting a hands-off approach.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but traded on exchanges like stocks, offering flexibility and diversification.

- Real Estate Investment Trusts (REITs): Companies that own or finance income-producing real estate, allowing individuals to invest in property without direct ownership.

Comparison of Stocks, Bonds, and Mutual Funds

Understanding the differences between investment types helps in making informed decisions. Below is a comparison table outlining key characteristics of stocks, bonds, and mutual funds:

| Investment Type | Risk Level | Potential Returns | Liquidity | Management |

|---|---|---|---|---|

| Stocks | High | High (long-term growth) | High | Self-managed or broker-assisted |

| Bonds | Low to Medium | Stable (interest income) | Medium to High | Self-managed or broker-assisted |

| Mutual Funds | Medium | Varies (depends on the underlying assets) | Medium | Professionally managed |

Assessing Risk Tolerance

Understanding your risk tolerance is a vital step in developing an effective investment strategy. Risk tolerance is the degree of variability in investment returns that an investor is willing to withstand. Factors influencing risk tolerance include age, income, investment goals, and personal comfort with market fluctuations. To assess your risk tolerance, consider the following aspects:

- Time Horizon: Longer investment periods often allow for greater risk, as there is more time to recover from market downturns.

- Financial Situation: A stable income and sufficient savings can increase your capacity to take on higher risks.

- Investment Goals: Define whether you are investing for short-term gains or long-term growth, as this will influence your risk profile.

- Emotional Comfort: Reflect on how you have reacted to past market declines. If you feel stressed during downturns, a conservative approach may suit you better.

Credit Management

Understanding credit management is crucial for maintaining financial health and achieving long-term financial goals. A good credit score can open doors to better loan terms, lower interest rates, and various financial opportunities. This section delves into the components that affect credit scores, provides techniques for enhancing personal credit ratings, and Artikels a responsible approach to debt management.

Factors Impacting Credit Scores

Several key components determine an individual’s credit score, forming the foundation of credit management. The major factors include:

- Payment History: This is the most critical factor, accounting for about 35% of your score. Timely payments improve your score, while late payments can significantly decrease it.

- Credit Utilization Ratio: This ratio, which represents the amount of credit used compared to the total available credit, constitutes 30% of your score. A lower utilization ratio is preferable.

- Length of Credit History: A longer history of responsible credit use can enhance your score. This factor accounts for 15% of your total score.

- Types of Credit: Having a mix of credit types, such as revolving credit (credit cards) and installment loans (mortgages, auto loans), can positively impact your score, comprising about 10% of it.

- Recent Credit Inquiries: Each time you apply for credit, a hard inquiry is made, potentially lowering your score for a short time. This factor is responsible for 10% of your credit score.

Techniques for Improving Personal Credit Ratings

Improving your credit rating is achievable through several strategic practices. The following techniques can help enhance your credit score over time:

- Make Payments on Time: Set up reminders or automate payments to ensure you never miss a due date.

- Reduce Credit Card Balances: Aim to keep your credit utilization below 30%. Paying off existing balances can have a significant positive impact.

- Limit New Credit Applications: Only apply for credit when necessary to avoid multiple inquiries that may lower your score.

- Review Credit Reports Regularly: Check your credit reports for errors and dispute any inaccuracies as they can negatively impact your score.

- Consider Becoming an Authorized User: Being added to a responsible person’s credit card account can improve your score, as long as they maintain good credit habits.

Guide for Managing Debt Responsibly

Managing debt responsibly is essential to maintain financial stability and protect your credit rating. Here are steps to consider when handling debt:

- Create a Budget: Track your income and expenses to understand your financial situation and allocate funds for debt repayment.

- Prioritize Debt Payments: Focus on paying off high-interest debts first while maintaining minimum payments on others.

- Communicate with Creditors: If you’re struggling to make payments, reach out to creditors to discuss potential payment plans or hardship options.

- Consider Debt Consolidation: Merging multiple debts into one loan with a lower interest rate can simplify payments and reduce interest costs.

- Seek Professional Help: If debt becomes overwhelming, consulting a financial advisor or credit counselor could provide valuable guidance and solutions.

Accounting and Auditing

Accounting and auditing are fundamental components of the financial landscape, acting as the backbone of informed decision-making in business and personal finance. Understanding the principles of accounting and the processes involved in auditing is essential for anyone looking to foster sound financial practices. This segment dives into the core principles of accounting, the auditing process, and discusses how accurate accounting impacts financial decision-making.

Fundamental Principles of Accounting

The fundamental principles of accounting provide the framework that governs how financial transactions are recorded and reported. These principles ensure consistency, reliability, and transparency in financial reporting. Key principles include:

- Accrual Principle: Revenues and expenses are recognized when they are earned or incurred, regardless of when cash transactions occur.

- Consistency Principle: Once an accounting method is adopted, it should be applied consistently unless a change is warranted and disclosed.

- Going Concern Principle: Financial statements are prepared under the assumption that the business will continue to operate indefinitely.

- Matching Principle: Expenses should be matched with the revenues they help to generate to provide a clear picture of profitability.

- Conservatism Principle: Anticipate no profits, but anticipate all losses, thus ensuring a cautious approach to reporting.

These principles form the foundation for credible financial reporting, allowing stakeholders to make informed decisions based on accurate and timely information.

Overview of the Auditing Process and Its Significance

Auditing is a systematic examination of financial statements and related operations to ensure accuracy and compliance with established standards. The process typically involves several key steps:

- Planning: Auditors assess the scope and objectives of the audit, including identifying the financial statements to be examined and determining the necessary resources.

- Fieldwork: This phase includes gathering evidence through various methods such as interviews, observation, and testing transactions for accuracy.

- Reporting: After completing the examination, auditors compile their findings into a report that highlights any discrepancies, compliance issues, or areas for improvement.

- Follow-up: Post-audit activities may include addressing identified weaknesses and ensuring that recommendations are acted upon.

The significance of auditing cannot be overstated; it provides assurance to stakeholders that the financial statements are free from material misstatements and that the organization operates within regulatory frameworks. An effective audit enhances credibility, strengthens internal controls, and fosters trust among investors and customers.

Impact of Accurate Accounting on Financial Decision-Making

Accurate accounting is crucial for effective financial decision-making. Reliable financial data enables organizations to assess their performance, manage cash flow, and plan for future growth. The impact of precise accounting can be illustrated through several key points:

- Informed Budgeting: Accurate accounting allows for the creation of realistic budgets, which serve as roadmaps for future expenditures and revenue forecasts.

- Investment Decisions: Investors rely on accurate financial statements to evaluate potential investments, making sound accounting practices essential for attracting capital.

- Compliance and Risk Management: Proper accounting ensures compliance with legal and regulatory requirements, minimizing the risk of penalties and fostering a culture of accountability.

- Performance Analysis: Financial reports derived from accurate accounting provide insights into operational efficiency and profitability, facilitating strategic adjustments.

In summary, the role of accuracy in accounting extends beyond mere number-crunching; it lays the groundwork for strategic decision-making, ultimately impacting the overall success and sustainability of an organization.

Banking Services

Banking services play a crucial role in managing personal finances effectively. Understanding the various types of bank accounts available and their respective benefits can empower individuals to make informed decisions about their money. Navigating through banking options with clarity leads to better financial management and maximizes the advantages of banking services.

Comparison of Bank Accounts

There are several types of bank accounts, each designed to meet different financial needs. Here’s a breakdown of the most common accounts and their benefits:

- Checking Accounts: These accounts are ideal for everyday transactions such as deposits, withdrawals, and bill payments. They usually come with debit cards and checks for easy access to funds.

- Savings Accounts: Savings accounts are designed for long-term savings, often offering interest on deposits. They are perfect for building an emergency fund or saving for specific goals.

- Certificates of Deposit (CDs): CDs offer higher interest rates in exchange for locking funds for a specified term. They are suitable for individuals who can set aside money for a while without needing immediate access.

- Money Market Accounts: These accounts typically provide higher interest rates and may offer check-writing capabilities. They are great for those who want to earn interest while maintaining some liquidity.

- Joint Accounts: Joint accounts facilitate shared financial responsibilities, making them useful for couples or business partners. They allow multiple individuals to manage and access the same funds.

Selecting Banking Services

Choosing the best banking services requires careful consideration of personal financial needs. When comparing banks and their offerings, the following factors should be assessed:

- Fees and Charges: Review account fees, transaction fees, and ATM fees. Opt for banks with low or no fees that align with your financial habits.

- Interest Rates: Compare the interest rates offered on savings accounts and CDs. Higher rates can lead to better returns on your savings.

- Accessibility: Consider the convenience of branch locations, ATM networks, and online banking options. A bank with extensive accessibility can save time and hassle.

- Customer Service: Evaluate the quality of customer support. Reliable customer service can greatly enhance your banking experience.

- Account Features: Look for features like mobile banking, budgeting tools, and alerts that can facilitate better management of your finances.

Understanding Bank Fees and Charges

Being aware of bank fees is essential for effective financial planning. Bank fees can quickly add up and impact your overall savings. Here are some common types of charges to keep in mind:

“Understanding bank fees can help you avoid unnecessary costs and ensure that you get the most out of your banking experience.”

- Monthly Maintenance Fees: Many banks charge a monthly fee for account maintenance. This fee can usually be waived by meeting certain conditions, such as maintaining a minimum balance.

- ATM Fees: Using an ATM outside your bank’s network often incurs a fee. Selecting a bank with a broad ATM network can help avoid these charges.

- Overdraft Fees: These charges apply when you spend more than your account balance. Having overdraft protection can mitigate these costs, but it’s important to understand how it works.

- Wire Transfer Fees: Sending or receiving money via wire transfer can incur fees, especially for international transfers. Be sure to check the rates before proceeding.

Financial Services

Financial services play a crucial role in helping individuals manage their money, plan for the future, and achieve their financial goals. These services encompass a wide range of offerings that cater to various aspects of personal finance, from banking to investment management. Understanding the financial services available can empower consumers to make informed decisions and optimize their financial well-being.

Types of Financial Services Available to Consumers

There are numerous financial services that cater to the diverse needs of consumers. Each service provides unique benefits that can assist individuals in their financial journeys. Here are some of the primary financial services readily available:

- Banking Services: Includes checking and savings accounts, loans, mortgages, and credit cards that facilitate daily transactions and long-term financial goals.

- Investment Services: Encompasses brokerage accounts, mutual funds, retirement accounts like IRAs and 401(k)s, and investment advice tailored to individual risk tolerance and goals.

- Insurance Services: Offers protection against unforeseen events through various policies, including life, health, auto, and property insurance.

- Wealth Management: Involves comprehensive financial planning and asset management for high-net-worth individuals, focusing on wealth preservation and growth.

- Tax Preparation Services: Assists individuals and businesses with tax planning, filing, and compliance, ensuring that they meet their tax obligations while maximizing deductions.

The Role of Financial Advisors in Personal Finance

Financial advisors serve as trusted professionals who help individuals navigate the complexities of personal finance. They play a pivotal role in crafting customized financial strategies that align with clients’ unique situations and aspirations.

“Financial advisors provide valuable insights and guidance that empower clients to make informed financial decisions.”

Advisors assist with various tasks, including investment selection, retirement planning, estate planning, and risk management. Their expertise can be particularly beneficial during significant life changes, such as marriage, buying a home, or planning for children’s education. Additionally, they help clients understand their financial situations better, enabling them to set realistic goals and develop actionable plans to achieve those goals.

Technology Transforming Financial Services

The advent of technology has significantly transformed the landscape of financial services, making them more accessible and efficient for consumers. Fintech innovations have reshaped how people interact with their finances, leading to a more streamlined experience.Key technological advancements include:

- Online Banking: Allows consumers to manage their accounts, pay bills, and transfer funds without visiting a physical bank branch.

- Mobile Payment Solutions: Enable instant transactions through smartphones, making payments more convenient and secure.

- Robo-Advisors: Automated investment platforms that create and manage portfolios based on individual risk profiles, often at lower fees compared to traditional advisors.

- Blockchain Technology: Provides enhanced security and transparency in transactions, particularly in areas such as cryptocurrency and smart contracts.

- Financial Apps: Offer budgeting, expense tracking, and investment tracking tools that help consumers stay informed about their financial health.

These technological innovations not only enhance the efficiency of financial services but also empower consumers to take control of their financial futures. As technology continues to evolve, it is expected to introduce even more innovative solutions that will further simplify financial management for individuals.

Credit and Collections

Credit and collections are critical aspects of personal finance management that can significantly impact your financial health. Understanding these processes and best practices can help you navigate the complexities of debt and improve your financial standing. This section delves into the intricacies of credit collection, ways to handle disputes, and the consequences of unpaid debts.The credit collection process involves several stages aimed at recovering debts owed to creditors.

Initially, a creditor will send reminders and statements to the debtor, highlighting the outstanding amount and due dates. If the debt remains unpaid, the creditor may escalate the situation by contacting the debtor directly through phone calls or letters. In some cases, a creditor may employ a collection agency to recover the debt, which introduces additional fees or penalties for the debtor.

The sequence typically includes:

- Initial Reminder: A reminder is sent via email or postal mail, detailing the overdue amount.

- Follow-Up Calls: If the debt remains unpaid, a representative may call the debtor to discuss payment options.

- Collection Agency Involvement: Failing to resolve the debt may lead to the assignment of the account to a collection agency.

- Legal Action: In severe cases, creditors may pursue legal action to reclaim the owed amount.

Best Practices for Handling Collections Disputes

When dealing with collections disputes, following best practices can help ensure that your rights are protected while resolving issues effectively. Disputes may arise due to various reasons, such as billing errors or discrepancies in the reported amount. It’s crucial to approach these situations strategically:

- Document Everything: Keep records of all communications, including dates, names, and the content of conversations.

- Review Your Credit Report: Check your credit report for any errors that might contribute to the dispute.

- Respond Promptly: If a collection agency contacts you, respond as soon as possible to avoid escalation.

- Negotiate Payment Plans: If you acknowledge the debt, consider negotiating a payment plan that works for both parties.

- Seek Professional Help: If disputes remain unresolved, consider consulting a consumer protection attorney for guidance.

The implications of unpaid debts on personal finance can be severe and long-lasting. Unpaid debts may lead to poor credit scores, which can affect your ability to secure loans, obtain credit cards, or even rent an apartment. Additionally, the accumulating interest on unpaid balances can escalate the debt significantly, making it harder to pay off over time. The stress of unpaid debts can also lead to negative emotional consequences, impacting your overall well-being.

It’s essential to understand these ramifications to encourage responsible borrowing and timely payments. Effectively managing credit and collections not only protects your financial future but also enhances your overall quality of life.

Personal Finance Management

Managing personal finances effectively is crucial for achieving financial goals, ensuring security, and enhancing overall quality of life. With the rise of technology, various personal finance apps have emerged to help individuals track their spending, set budgets, and plan for the future. Additionally, financial literacy plays a key role in understanding how to manage money effectively, making informed decisions, and fostering a sense of control over one’s financial situation.

Regular financial check-ups are also essential to stay on track and adjust plans as necessary.

Personal Finance Apps and Their Features

In the digital age, personal finance apps serve as valuable tools that simplify financial management. Here’s a list of popular apps along with their notable features:

- Mint: This app offers budgeting tools, expense tracking, and bill reminders. It provides insights into spending habits and helps users create financial goals.

- YNAB (You Need A Budget): Focused on proactive budgeting, YNAB helps users allocate every dollar of their income and emphasizes the importance of saving for future expenses.

- PocketGuard: This app simplifies budgeting by showing how much disposable income you have after accounting for bills, goals, and necessities.

- Personal Capital: This offers both budgeting and investment tracking features, allowing users to manage their net worth and assess their investment performance.

- GoodBudget: Based on the envelope budgeting method, this app allows users to plan their spending and track their budgets across multiple devices.

Importance of Financial Literacy in Personal Finance

Financial literacy is the foundation of effective personal finance management. It encompasses understanding financial concepts such as budgeting, saving, investing, and credit management. Being financially literate empowers individuals to make informed choices, avoid debt traps, and plan for future needs. For instance, understanding the implications of credit scores can significantly impact borrowing costs and access to loans.

“Financial literacy is not just about knowing how to balance a checkbook; it’s about understanding the broader financial landscape and making informed decisions.”

Framework for Regular Financial Check-Ups

Establishing a framework for regular financial check-ups is essential for maintaining financial health. These check-ups allow individuals to review their financial situation, assess progress toward goals, and make necessary adjustments. A basic framework could include:

- Monthly Budget Review: Evaluate your budget each month to see if you are sticking to your spending limits and identify areas for improvement.

- Quarterly Financial Goals Assessment: Every three months, review your financial goals to determine if they are still relevant or need adjustments based on changes in income or expenses.

- Annual Credit Report Check: Request your credit report annually to ensure accuracy and address any discrepancies, which can affect credit scores.

- Investment Portfolio Review: At least once a year, assess your investment portfolio’s performance and reallocate assets as needed based on market conditions and personal goals.

- Emergency Fund Evaluation: Regularly check if your emergency fund is adequate to cover at least three to six months of expenses, adjusting contributions as necessary.

Final Conclusion

In conclusion, adopting smart money habits can pave the way for a secure and prosperous financial future. By budgeting wisely, planning effectively, and investing intelligently, you can navigate the complexities of personal finance with ease. Remember, the journey to financial stability is a continuous process, and the habits you cultivate today will serve you well in the years to come.

Top FAQs

What are smart money habits?

Smart money habits are practices that help individuals manage their finances effectively, leading to better financial stability and growth.

Why is budgeting important?

Budgeting helps you track your income and expenses, enabling you to make informed financial decisions and avoid overspending.

How can I improve my credit score?

Improving your credit score involves paying bills on time, reducing debt, and monitoring your credit report for errors.

What is the purpose of an emergency fund?

An emergency fund provides financial security by covering unexpected expenses, reducing the need to rely on credit or loans.

How often should I check my financial progress?

It’s recommended to review your financial situation regularly, at least once a month, to stay on track with your goals.